Everything You Need to Know About Seller Financing

When it comes to buying a small business, especially your first one, coming up with the cash can be the biggest hurdle to overcome. Seller financing may be your key to making it happen.

Small business seller financing is a type of financing where, instead of getting a loan from a bank or other financial institution, you get the financing directly from the seller.

It allows you to negotiate flexible payment terms and gives you more control over your investment while avoiding a large down payment.

This is what I’m talking about when I say you can buy a business with other people’s money by financing your purchase with future sales.

But how exactly does seller financing work?

Basically, the seller gives you a loan to purchase their business instead of expecting full payment upfront.

This gives cash-strapped buyers an opportunity to purchase a small business that they otherwise couldn’t afford and allows both parties to benefit from the transaction in an equitable way.

Sound too good to be true? Good instincts. There are risks involved, so make sure you understand the ins and outs of seller financing before deciding if it’s right for your situation.

Structuring a seller financing agreement

Understanding how to structure a seller financing agreement is essential. You’ll want to discuss each of these factors with the seller before drawing up an agreement:

- Down payment: How much are you putting down at closing for the business?

- Interest rate: Annual rate of interest that will be paid to the seller on the note. Note whether this is a fixed or variable rate.

- Term: How long you have to pay back the loan with a payment schedule.

- Security or guarantees: What sort of guarantees does the seller have that they will get their money?

Benefits and risks of using seller financing

We’ll start with the bright side.

Benefits:

- Faster closing: With seller financing, you can skip all the red tape and waiting around for a bank loan officer to approve your application. You can get to the good stuff faster, like owning your dream business.

- Cheaper closing costs: Who wants to pay a bunch of fees and appraisal costs? Not me, and I bet not you either. With seller financing, you can avoid all those extra costs traditional lenders like to charge.

- Flexible down payment: You can negotiate with the seller for a more flexible down payment without worrying about strict bank or government-required minimums. It’s like having a personal finance genie at your disposal.

- Easier financing: Can’t get approved for a loan? No problemo. With owner financing, you don’t have to subject yourself to the strict loan approval procedures that traditional lenders use. However, the seller will likely run a credit check on you, so make sure you’ve been paying your bills on time.

Potential risks:

- Personal guarantees: One of the major risks associated with seller financing is that it often involves personal guarantees. This could make you liable for debts incurred during the transaction as well as any future loans related to the business.

Personally, I would push for the seller’s only recourse for failed payment to be to take back the business. This de-risks the deal for both you and the seller. In a worst-case scenario, the seller gets to keep whatever they collected and step back in to right the ship. They can even sell the business to a new buyer if they want.

- Higher interest rates: Buyer beware – many sellers opt for high interest rates in order to increase their return from a sale and make it more lucrative.

I would try to frame the interest rate based on what the seller believes they could earn elsewhere rather than against competitive SBA rates. If you pitch this correctly, you can persuade the seller of the benefits of offering seller financing. Otherwise, they need to find a place to invest the cash to generate a similar return after the sale.

- Higher overall cost: Keep the phrase “My price, your terms or your price, my terms.” in mind. You may end up paying a little more for the business, but you get to make the purchase without putting down all of your cash.

Tips for negotiating terms

So, let’s talk about terms. When negotiating seller financing terms, it’s important to create a win-win situation for both parties. You want the best possible deal that limits your personal financial risk while still being attractive to the seller.

Obviously, most sellers would like as much money as possible from the deal. But you would be surprised at how many other factors come into play here. Knowing which levers to pull can land you much better terms, while also making the seller feel secure in the deal.

Start by opening up a dialogue to understand the seller’s ideal outcome. Here are a few questions I like to ask:

- What’s most important to you in selling the business? (Success of the business after the sale, clients being well taken care of, employees having jobs, cash received immediately, or total cash received over the next few years?)

- How do I make this a win for you?

- If I paid you the total amount today to buy the business, what would you do with the cash?

- Have you talked with your accountant about how to handle the taxes from a big lump sum payment?

- What rate of return do you think you could get with cash in a safe investment vehicle right now if you were to invest it yourself?

Then, research best practices and seek expert guidance to gain an understanding of the legal and tax requirements associated with the transaction. Better yet, hire a lawyer.

When you present facts rather than speculations, you put yourself in a stronger position and increase your chance of getting the best deal possible.

Learning how to negotiate the best terms for your seller financing deal can save you significant time, money and effort in the long run.

Sourcing funds to finance a seller-financed deal

When considering how to source the down payment for your seller-financed small business purchase, you’ve got options. Perhaps the most traditional option is to use funds from personal or retirement accounts.

But there are also other sources to consider, like outside private funding and investments, partnerships, friends and family members. Loan officers and financial advisors can offer expertise and help evaluate your specific situation.

It all comes down to finding the best balance of risk and reward. Getting creative with down payment sources can be one way to increase profitability while lowering the overall costs associated with the purchase.

If you find a motivated seller and really turn on the charm, you may even negotiate the down payment to nothing – like this 22-year-old who bought a car wash that now cashflows $7.4k a month.

With seller financing, you’re basically using other people’s money and buying a business with little to no money down. What’s not to love?

Of course, there are risks involved with this type of transaction, but nothing you can’t handle with due diligence and skillful negotiation.

If you need a confidence boost, check out our course on how to buy a small business.

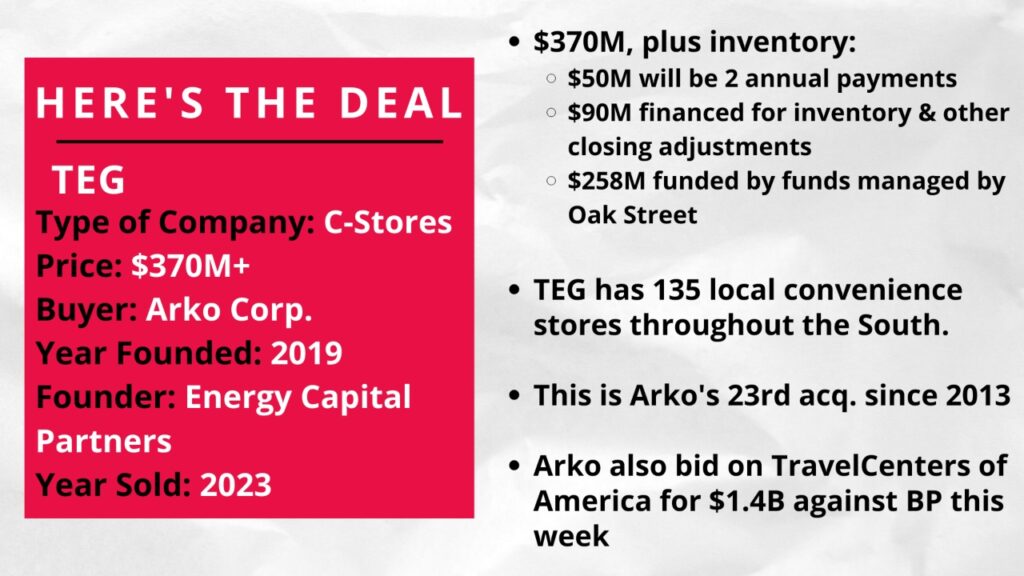

This Week in Biz Buying:

Lessons the big acquisitions can teach you about YOUR deals

❤️ CVS buying provider Signify Health for $30.50/share, or ~$8B total

Underrated (un-fur-rated?) recession-resistant sector: pet retail

The $44B purchase now worth $20B (but is $250B in its future??)

☕ Starbucks‘ new union-busting strategy: make the CEO a barista