Everybody stay calm

So you just signed on the dotted line for your first 7-figure biz deal. You should feel totally relieved because the hard part’s over, right?

Hardly. Because deep down, you know that the real work has just begun.

You might be feeling in over your head with a big ol’ side of buyer’s remorse. (Or at least, “holy sh*t did I really just do that?!”)

You probably also feel a little overwhelmed by all of the new items on your to-do list, thinking “there’s no way all of this is gonna get done.”

Keep your eye on the ball and take it one day at a time.

I remember the first time I secured my first 7-figure deal. I called my husband, then felt like throwing up in my mouth a little bit.

But you don’t have to play small or play scared. You just need to go into the first 90 days of your new business with a plan.

Which is why we’re giving you a checklist of where to focus during the first 90 days after your business deal goes through.

But first, let’s back up a little.

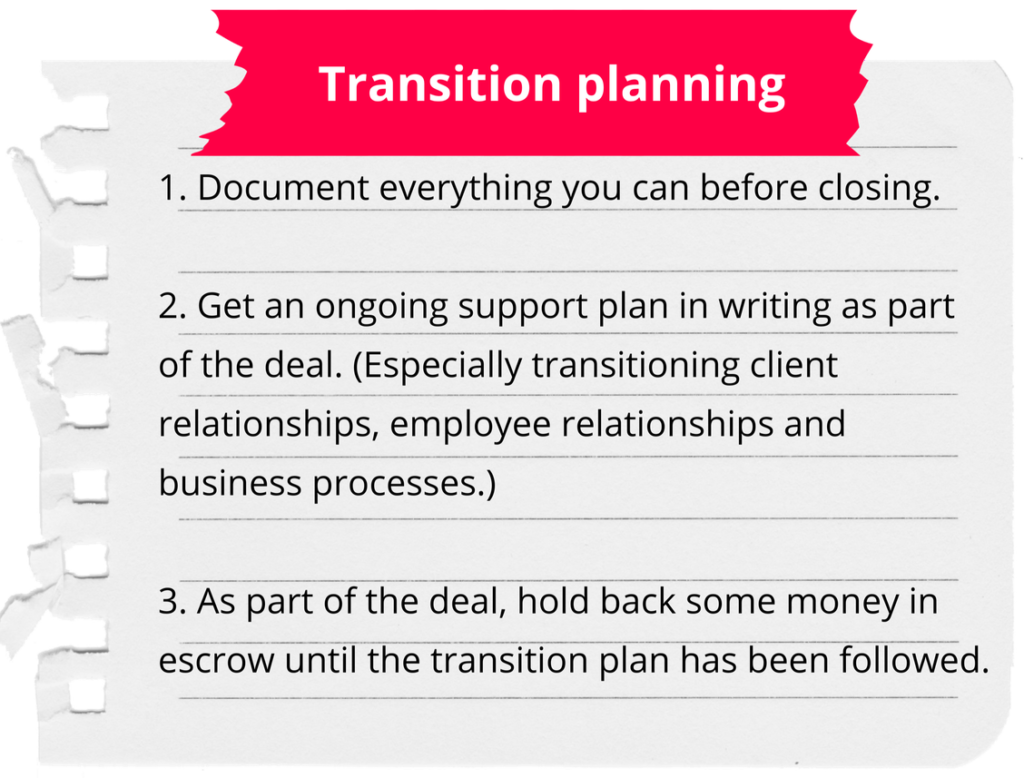

Transition plans start before closing

The success of your transition often hinges in what you can accomplish with the prior owner before the closing date.

Remember, they are often looking to retire. And while helping you make a successful transition may sound great in the beginning, if it’s not part of the agreement and the payday, they may soon forget all about you.

Negotiate for as much of the seller’s knowledge and key employee knowledge to be documented before the closing. Work with them to make sure you get everything you need.

Our friend Lisa Song paid $10,000 just to follow an owner around their store for 2 weeks to write out her playbook. These systems are the key to owning a passive business.

Here are 3 quick tips to get the most out of the relationship with the seller before they move on with their lives:

How to spend the first 90 days

Not trying to turn this into a Tony Robbins kumbaya sesh, but if there’s one thing you need to know about the first 90 days in your new business, it’s this:

The first 90 days will make or break you.

Taking the time to plan and prioritize during the first 90 days is essential for long-term success. Some of the big milestones and biz health checks you’ll be up against are:

- Transitioning the previous owner completely out of the business

- Communicating the sale with the public (i.e. customers, employees and possibly investors)

- Hiring and training your operator

- Highlighting SOPs that still need to be documented

- Assessing the general health of the business (i.e. cash, MRR, expenses and profit margin)

- Setting monthly, quarterly and yearly goals

- Shadowing and interviewing managers and employees

- Introducing yourself to any additional contractors or service providers you’ll work with directly

- Familiarizing yourself with the backend of the business (i.e. the tech, software and systems)

- Redefining the company culture, especially if there are any significant changes from the previous ownership

- Surveying and reorganizing the current org structure (including promoting or dismissing current employees)

- Implementing or remixing your marketing plan

- Adding an additional product, service or other revenue stream to your current business services

- Launching a customer retention or referral program (if there’s not one already)

I know it looks like a lot, but Rome wasn’t built in a day, either. The biggest piece of advice I can give you is to create a clear plan for which tasks you’ll tackle every 30 days of the transition period.

And if you have a team…by all means delegate!

Who’s the boss?

You may be tempted to show up guns ablaze from the very beginning, but hold your horses, cowboy.

The most productive way to spend your first 30 days is by being a fly on the wall and listening.

There is a lot of tribal knowledge floating around your business. Leverage it. You don’t have to sit there trying to figure out how to reinvent the wheel when you’re surrounded by folks who have been doing the work for years.

You’ll also want to show the employees you inherited that you are someone to be trusted.

I’m also not gonna sugarcoat this next part: managing people is hard AF. Even when you think you know exactly what you’re doing, people are unpredictable. So brace yourself, my friend.

But even if you’re new to managing employees, you don’t have to do anything too drastic to win their trust. People be smart, and they can sense when you’re full of sh*t. Be real. Be honest.

Asking their opinion on what could be improved is a great start to grease the wheels.

As you work through conversations with your employees, always carry a notebook with you (or take notes in your phone). It shows you actually care what they think.

Some of the best Qs to ask employees:

- How long have you been working here? Why did you first want to work here?

- What do you think our biggest strengths and weaknesses are as a company?

- What are your career aspirations? Is there anything that’s missing for you here?

- If I could wave a magic wand and change one thing in the company overnight, what would it be and why?

- If we had endless time, money and resources, what is one thing you think we should start doing? What do you think should stop?

- What is the most common customer complaint you hear about? Why do you think that’s the case?

Talk to customers and vendors

Speaking of customers…

When you take over ownership of a business, it’s essential to have conversations with both your customers and vendors to understand their expectations and needs.

Ask questions like:

- What do you value most in our products or services?

- What do you want more of?

- What do you like least about the current purchase experience?

Taking the time to listen and learn from customers and vendors helps build relationships that stand the test of time.

Working together openly, honestly and transparently will ensure that any customer issues are addressed quickly. It also creates trust that could lead to repeat purchases or long-term contracts.

At the end of the day, your goal is to understand their wants and needs so you can make informed decisions based on sound data points.

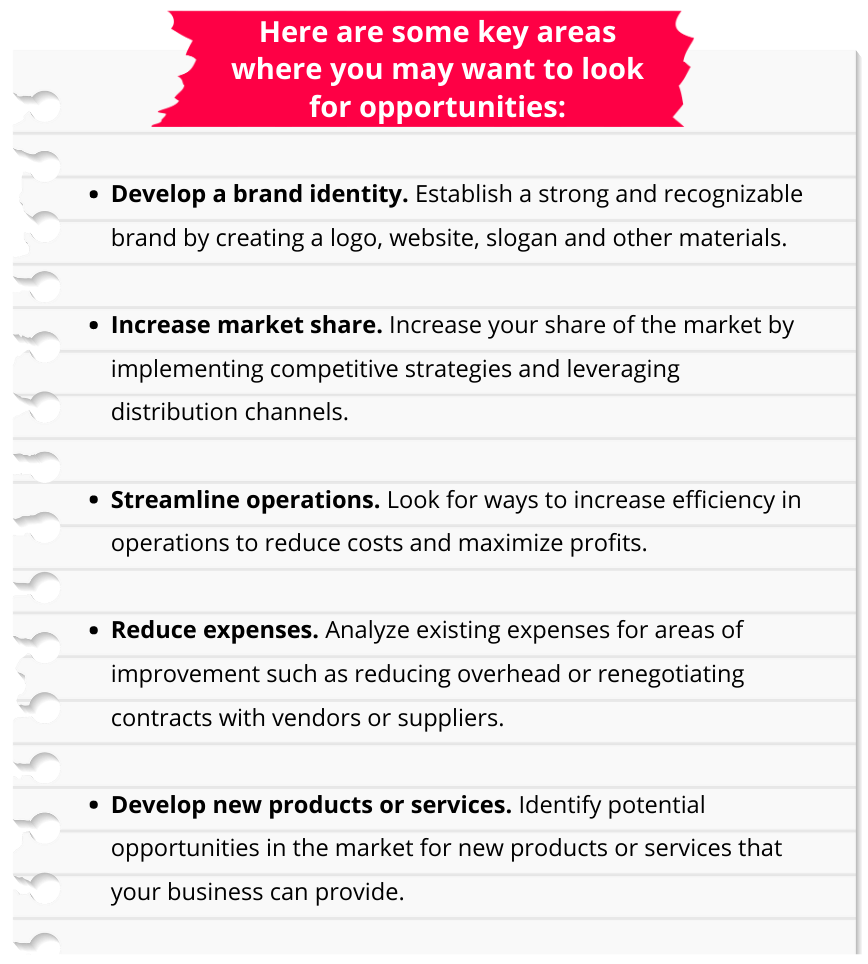

Establish goals and strategies

Now that you’re in charge, it’s time to set the course. Figure out what you want to achieve and decide on your timeline.

Set achievable milestones with realistic budgets and be sure to include contingencies in case of setbacks or surprises – because, oh yes, there will be setbacks and surprises!

Don’t forget to factor in any external factors, such as regulations or market trends, that could affect outcomes.

It pays to embrace unconventional thinking too. (Let’s be honest, it usually does.)

Consider taking some calculated risks, investing in marketing campaigns, expanding into new markets or even developing some alliances.

These approaches may not be everyone’s go-to, but they could be just the thing to give your business a competitive edge.

We teach a tool called the 3-M Model to determine which areas make the most sense in growing your new business.

Markets, marketing channels and media.

Once you have everything figured out, it’s time to put your strategy into action.

Make sure everyone involved follows through, and keep reviewing progress over time so any changes can be implemented quickly.

Understand your processes

This part puts the ‘B’ in boring businesses for me, but it also puts the ‘B’ in billion-dollar companies.

A great approach for capturing processes is creating a core processes map with the former owner as part of the transition plan.

Break the business operation into 5 to 7 core processes. Then create how-to instruction manuals for each of the major tasks in those core processes.

If new technologies or regulations have been introduced since you took over, ensure that they are documented, too.

Include tests and quality assurance checks – you don’t want to end up with incomplete documents and gaps in understanding.

Test each process by having someone follow the guide and complete the task. Make updates where the outcome doesn’t match what was expected.

If this task feels too daunting, you can assign it to someone on your team who has an enthusiasm for details. They can bear the brunt of the paperwork and take on the challenge of accurately capturing these processes.

Planning creates profit

It’s likely that you’ll enter into your first 90 days with more Qs than you know what to do with.

Again…this is to be expected.

But as long as you also go in with a plan, your first 90 days can help you set up your business and your team to see a lot of success.

In fact, the plan you put into place during your first 90 days will likely impact your profitability (as well as your cashflow) for the next 12 months.

But get it wrong, and you’re looking at employee turnover, finding a new operator, or draining thousands of dollars on new policies and procedures that you didn’t need in the first place.

Go slow. Stay steady. And keep it unconventional.

Deal of the week: A Total Win

This Week in Biz Buying:

- Food co.’s are buying, it’s paying off

- 2 strong meat brands acquired

- Buffett’s casual $8.2B acquisition

- Hotels expanding into glamping